In lieu of the typical jobs report, here’s a look at some other data points that portend where industry is going.

How is manufacturing doing in America? While we don’t have the September jobs data in hand just yet, the answer is surprisingly boring, especially given some of the rhetoric and biased analysis you may be seeing or hearing. “Boring” is a description unlikely to please some Democrats, who are focusing on recent declines in manufacturing jobs to argue the sector is in serious trouble, or many Republicans, who have been heralding announcements of new factories under construction as evidence of a boom.

Let’s look at four useful hard data sets to paint a better picture.

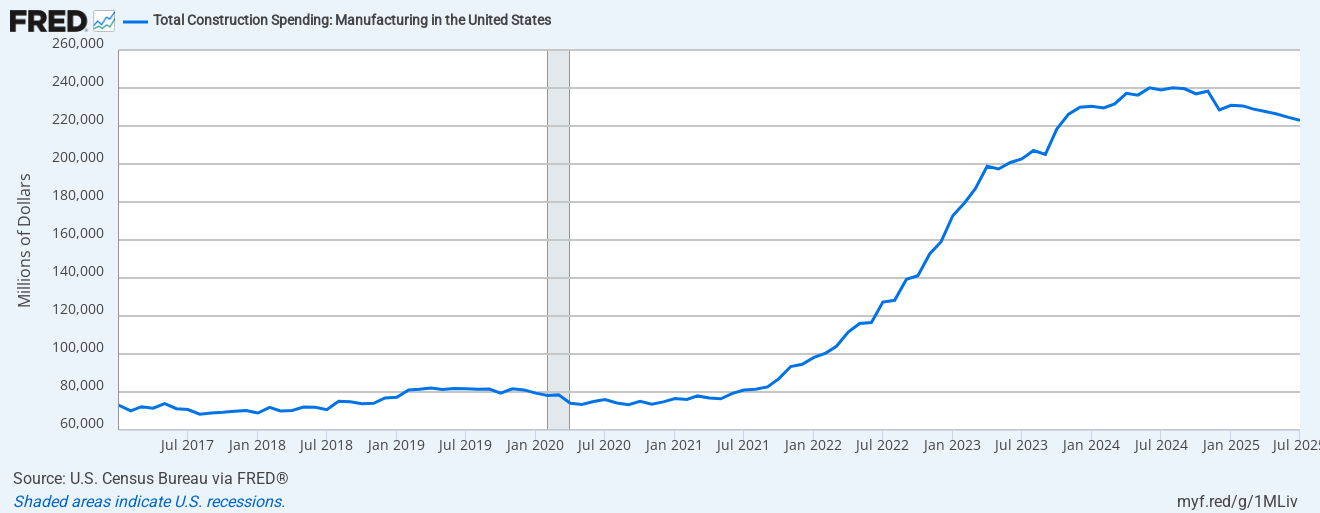

First up, factory construction.

There’s been a massive surge in spending on factory construction since the end of 2021. The reasons for this upswing include companies proactively locating (or in some cases reshoring) production in the U.S. to avoid supply chain challenges, as well as major incentives provided by public investment in sectors such as semiconductors and renewable energy products. And while new factory construction spending peaked about a year ago, it’s still extremely high. In fact, the latest reading is about three times the average level of factory construction in the years prior to 2021. While the composition of that construction may be shifting — think less in renewables and more in pharmaceuticals — the level of investment is still impressive.

Will finalizing the tariffs help unlock additional factory construction? It’s quite possible, but that will depend in part on how high tariff levels remain in certain sectors that can be reshored.

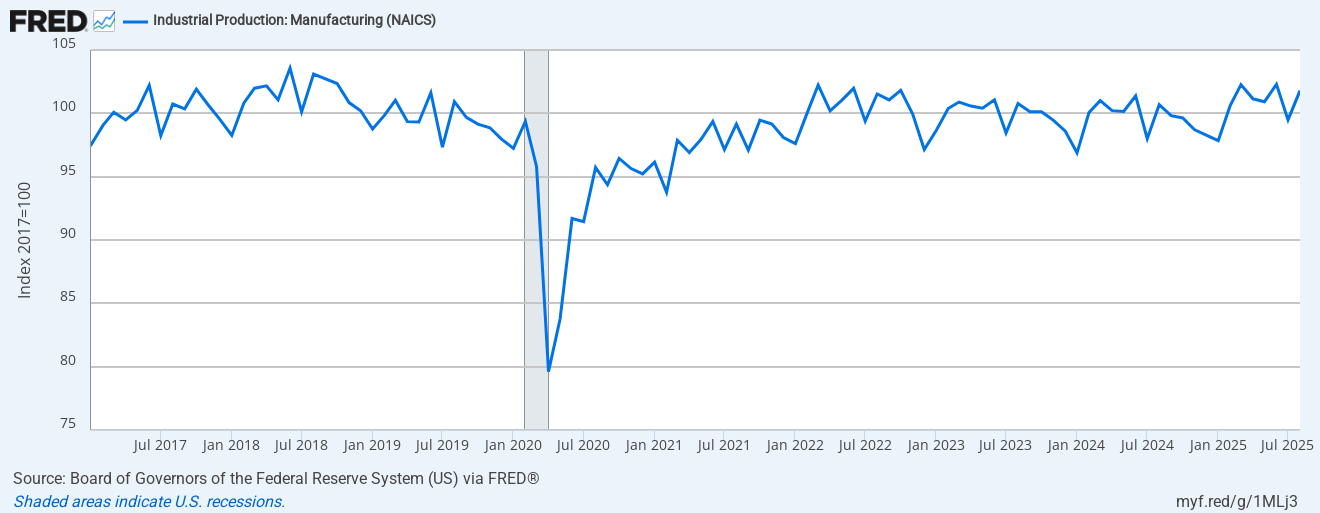

Next, let’s look at industrial production in the manufacturing sector.

Since January 2022, that number has been hovering just above or below the baseline established back in 2017. It’s been slightly expanding in some readings and contracting in others. The most recent reading — from August of this year — was in positive territory. Steep plunges in this index are correlated well with recessions, but we haven’t seen any evidence of that yet. If anything, the index is showing signs of a rather stable factory sector.

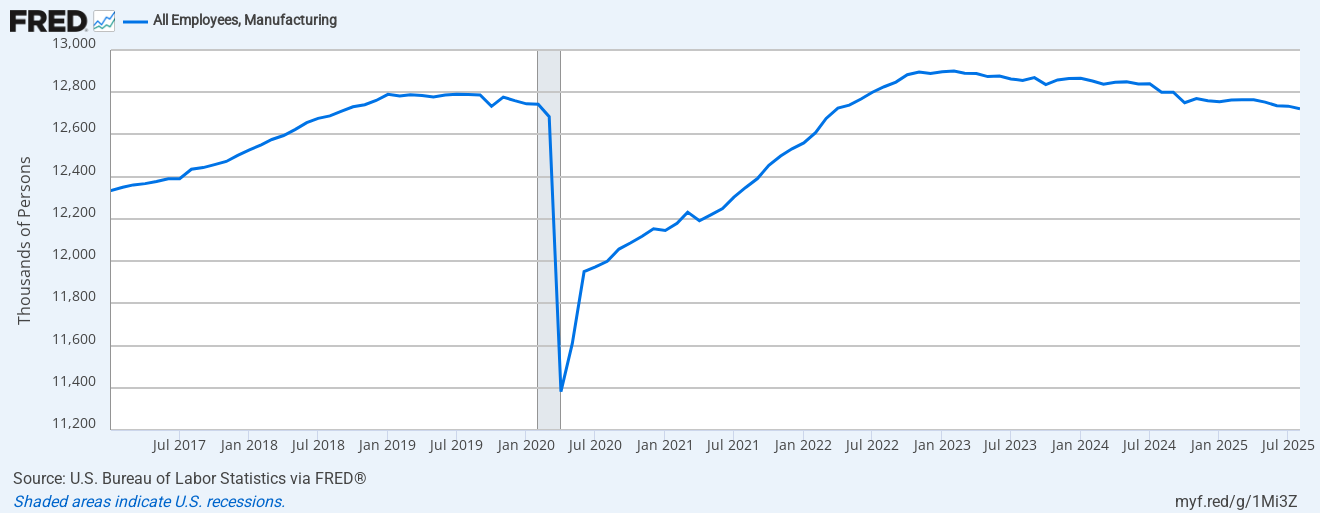

Let’s move on to manufacturing jobs.

We don’t have September jobs data yet, but we can look back and draw some reasonable conclusions. First, the sector is treading water when it comes to employment and has been for some time. Manufacturing jobs reached a post-pandemic peak in February 2023 and the trend since then has been a very gentle decline. So, no matter what you may see or read from pundits and politicians, this is not a boom, nor is it a bust. The downward trend is concerning, however, as the trend from 2010 to 2018 was a gradual upswing. Several reasons have been put forward as to why we’ve seen stagnation, including higher tariffs, interest rates, tariff uncertainty, availability of workers, weakening consumer demand, and/or increased productivity. But it’s way too early to tell what the primary driver is.

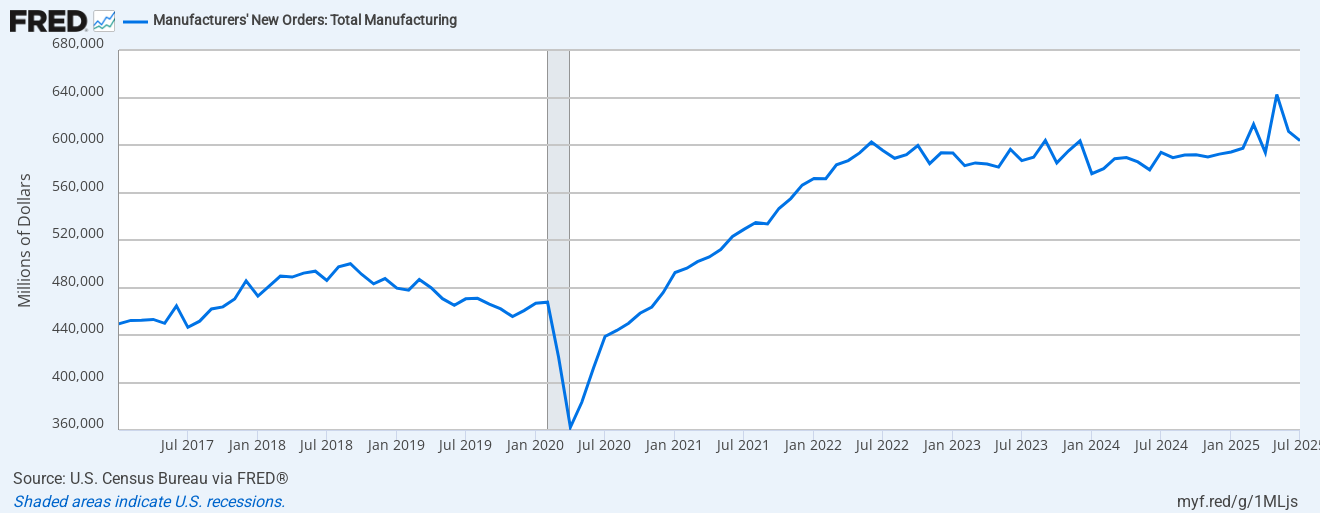

One big indicator of what the future for factories may look like is new orders.

This data represents the volume of new purchase orders placed with manufacturers, and it has stayed within a narrow range of $570 to $605 billion over the past three-plus years with a little more volatility over the past few months. During times of recession, this data point drops like a rock. We just haven’t seen that happen yet.

I want to acknowledge that I have not included trade data, in part because the volume of imports has been impacted by stockpiling in anticipation of tariffs. If the tariff policy is working down the road, the trade deficit in goods should be declining. If the trade deficit is not coming down at that point, it means that either the dollar has appreciated (partially offsetting the rise in import prices) or that the tariffs are not deep and broad enough to be impactful.

I’m rooting for more factory jobs, but we just aren’t seeing them yet. Wait a few months for interest rate reductions to kick in, tariffs to become more permanent, and several aspects of the tax code (expensing and depreciation) to show up in the data. Then we’ll have something to talk about.